The Great Awakening-In God We Trust

Deflationary Tsunami On Deck: A "Tidal Wave" Of Discounts And Crashing Prices

Gwen Baer says she now wishes she had waited before splurging on a $3,000 couch for her new home that took six months to arrive in 2020. The 30-year-old Atlanta digital-media strategist plans to watch for sales at Target, West Elm and other retailers to finish outfitting her house, which she and her fiancé purchased in August 2020.Her fiancé, Thomas Li, hopes to buy a new TV to replace the 10-year-old one in their bedroom. He’s hoping the sales mean lower prices on OLED screens.“The stores are really making lemonade out of some lemons,” Ms. Baer says.

Views: 5

Comments are closed for this blog post

-

Comment by carol ann parisi on June 18, 2022 at 7:20pm

-

"The Country Is Going To Learn That A Recession Is Worse For Votes Than High Inflation"

By Peter Tchir of Academy Securities

Be Careful What You Wish For

The market basically begged the Fed to hike 75 bps (to prove that they are fighting inflation) and hoped Powell would be just dovish enough during the press conference to alleviate some fears in risk assets.

The market got what it wanted and responded accordingly, finishing near the best levels of the day. We wrote to fade that, though how quickly the sell-off hit and ugly it is, surprised us.

In any case, the market got what it wished for, but maybe, just maybe, hiking 75 bps into a rapidly weakening economy isn’t the best idea.

Last weekend’s T-report moved our economic outlook to DEFCON3, I expect to make it worse in this weekend’s report (DEFCON2).

A few quick things making me particularly nervous:

75 bps will hit earnings, will hit adjustable rate mortgages, etc.

The ECB, for anyone who lived through the European debt crisis, only acts, once it has failed to act repeatedly and markets hold their feet to the fire to the point that the smell of burning flesh nauseates those holding their flesh to the fire. (they seem to be leaning towards selling some assets to buy Italian bonds, certainly not the bazooka the market was hoping for after an emergency meeting).

The wealth destruction has been enormous. Stocks in general have been hit hard (the S&P 500 down by 20%). But megatech has been hit worse, and there has generally been carnage is disruptive stocks, recent IPOs and SPACs. Bonds have not provided any respite and 60/40 funds have been failing their clients. For the past week or so, even commodities haven’t ridden to the rescue (XLE is down more than 10% in just over a week). Crypto is also hitting people’s wealth hard (at least those exposed to it) with Bitcoin’s “only” 70% drop from November highs, being the envy of most of the alt-coins. Even housing, I find it difficult to believe that many purchases in the last 3 months are above water, and owners who thought about selling are well aware of this hit to their capital.

Liquidity is abysmal in and across asset classes.

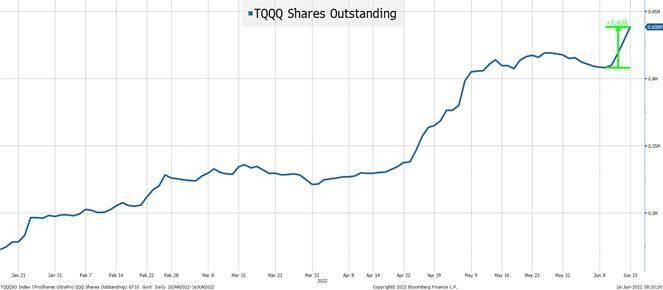

This Chart Bothers Me

TQQQ is once again seeing some serious dip buying. Shares outstanding have increased by 7% in the past few days, bringing the total market cap to $10 billion (representing $30 billion of risk, since it is 3x leveraged). The market cap would be bigger, but the share price has declined so much, that each new dollars creates more shares.

For some reason, I keep gravitating to this data point, because I can’t get it out of my head that it is likely representative of whether we’ve capitulated or not.

I believe that the country is going to learn that a recession is worse for votes than high inflation and the 75 bp hike likely speeds along some of the many issues facing the economy.

Biden about to find out what polls worse: recession and bear market or runaway inflation.

— zerohedge (@zerohedge) May 20, 2022What is disturbing is how easily the sovereign debt markets (including Treasuries) fall into disarray. My fear of a shock in the bond market, some sort of “flash crash” is increasing yet again, as overnight trading was bad and not reflective of recessionary views.

In hindsight, what the market cheered for yesterday, will be viewed as a bad outcome (and that is without a single Fed speaker hammering home the inflation fighting stance, which is likely to come now that the blackout period is over)

More in this weekend’s DEFCON2 report.

About

© 2025 Created by carol ann parisi.

Powered by

![]()